Hidden Alpha: Exploring Value in a Crowded Market

Thoughtful Investing for Long-Term Wealth Creation

Disclaimer:

The following content is for informational and educational purposes only. It reflects my personal investment philosophy and experiences and is not intended as investment advice. Please consult a SEBI-registered financial advisor before making any investment decisions.

Hello Investors,

I'm excited to share my thoughts with fellow investors who share my passion for long-term value investing. My goal is simple: to encourage and inspire the practice of thoughtful, patient investing.

My guru Mohnish Pabrai, and his inspirations are none other than Warren Buffett and Charlie Munger. Throughout this letter, you'll see me refer to lessons from all three—masters of compounding wealth over the long term.

The Landscape of Investing Today

Investing today is more competitive than ever, with more participants and access to more information than at any time in history. For instance, during the time Buffett's "Superinvestors" were making their mark, obtaining annual reports involved requesting them by mail—sometimes waiting weeks for a response. Today, a few clicks allow you to download that same report instantly. The number of analysts tracking stocks has skyrocketed, making the field even more crowded.

While I don't believe that markets are entirely efficient, the room for extraordinary outperformance is certainly smaller. As Charlie Munger often advises: "Invert, always invert." If we ask which assets face less competition and scrutiny, we might find a path less trodden. Personally, I find that small-cap companies to generate outsized returns. These companies often have fewer analysts covering them simply because large funds cannot take significant positions. This allows us to take advantage of opportunities with less competition, at least until the fund grows to an extent where investing in small-cap companies becomes problematic.

Investment Style

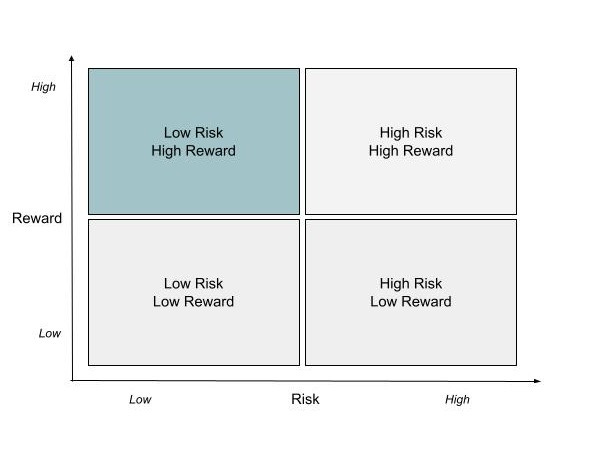

We always feel that risk is correlated to reward, but there is an investing style that my guru, Mohnish Pabrai, has taught me: "Heads I win, tails I don’t lose much." If we break the risk-reward trade-offs into a 2x2 grid, we can see four scenarios:

Low Risk, Low Reward: These include mature stocks such as large banks or IT companies, where growth is stable and predictable. Growth rates are largely factored into the price, and such stocks often appreciate in line with the overall index or GDP growth.

High Risk, Low Reward: These are typically the stocks that retail investors chase when they are in vogue with market trends. Retail investors often ignore valuations and are driven by the stories behind these stocks. Historically, these have not yielded great returns.

High Risk, High Reward: These could be leveraged positions, contrarian bets, or turnaround stories. Vodafone idea, for instance, could fall into this category (though some might argue it is high risk with low reward).

Low Risk, High Reward: This is where I like to operate. These are stocks that may be beaten down due to a few bad quarters or that have been misunderstood by the market. They might also be stocks that analysts ignore entirely. In my experience, such opportunities are poised for growth in the coming quarters. As the growth materializes, the stock price often returns to its fair valuation, providing significant upside without excessive risk. This approach embodies the philosophy: "Heads I win, tails I don’t lose much."

Attributes for Successful Investing

I believe that the key to generating wealth lies in a few core principles. Let me expand on them here:

Price vs. Value: As Aswath Damodaran famously says, "Price is what you pay, value is what you get." I look for stocks that offer a clear disparity between these two—paying a fair or undervalued price while expecting robust growth in value. Our goal is to purchase undervalued opportunities with long-term potential, avoiding the irrational exuberance that often inflates prices beyond reason.

Simple to Understand Businesses: Complexity is often the enemy of good returns. Like Warren Buffett says, "Invest in businesses that even an idiot can understand, because sooner or later, one will run it." Our focus is on companies whose business models can be explained to a Grade 3 student. Simple, well-run businesses often yield reliable results over time.

Holding for the Long-Term: Buffett's holding period, as he famously says, is "forever," as long as the underlying thesis holds true. Similarly, I aim to hold companies as long as they continue to fulfill our original investment thesis. We only sell if the business fundamentals deteriorate or the valuation becomes significantly overblown.

Concentrated Bets: I believe in investing heavily in my best ideas. Concentration allows me to take meaningful positions when conviction is high, even though it may involve a higher degree of perceived risk.

One-Person Investment Committee: Investment by consensus can lead to mediocrity. I believe in the strength of independent thought. My process involves generating ideas on my own. You may agree or disagree with my thesis, but a consensus-driven approach dilutes the potential for real conviction.

Mistakes & Risks

Warren Buffett recently reminded us that mistakes are part of the journey. Out of roughly 800 investments he’s made over decades, he attributes most of his success to just a few—like Coca-Cola, Bank of America, and Apple. In his annual letter, he acknowledged that the majority of his investments were unremarkable, but those few successes made all the difference.

The lesson here is humility. Personally, I focus on learning from mistakes. Not every stock will be a winner, and there are no guarantees of outsized returns. But I will continue striving to beat the market, remaining open to learning from mistakes, and focused on the process rather than just the outcome.

If you believe in the value of long-term investing, I invite you to join me on this journey. Over the next few days, I plan to share detailed investment theses on the stocks I currently hold—my high conviction bets. I’ll explain why I own them, the rationale behind my decisions, and their potential to deliver outsized returns.

Sign up to stay updated and receive my latest articles directly in your inbox. Let’s explore the art of thoughtful, long-term investing together.

Explore More Investment Ideas

If you found this article helpful, check out my other analyses, and subscribe to get notifications for my posts:

Unlocking the Potential of Ashiana Housing: A Small-Cap Gem in Real Estate (NSE: Ashiana)

·Ashiana Housing is a small-cap real estate developer in India with a diversified presence across Rajasthan, Pune, Delhi, Chennai, Jamshedpur. Operating primarily in the premium residential segment, Ashiana focuses on constructing 2/3 BHK apartments priced around INR 80 lakhs to 1 crore. Their core offerings are chi…

BestAgro: Positioned for Growth Amid Favorable Agricultural Trends (NSE:Bestagro)

·BestAgro is a fertilizer manufacturing company based in India, operating in a niche with significant growth potential. The company transitioned from manufacturing technicals and formulations for larger brands to producing its own branded products in 2022, thereby unlocking higher margins. Alongside its manufacturing and co…

Edelweiss Financial Services: Unpacking Growth and Value Potential (NSE: Edelweiss)

·Edelweiss Financial Services is a diverse conglomerate with a focus on financial services in India. It has recently been making waves in its value unlocking strategy, with the successful spin-off of Nuvama being a key milestone. Led by Rakesh Shah, Edelweiss consists of five main business verticals:

Regards

Let me know your comments here

Does category of risk and rewards depends on the sector like IT or banks? I think it’s more depends on the company.